Managerial accounting vs cost accounting management

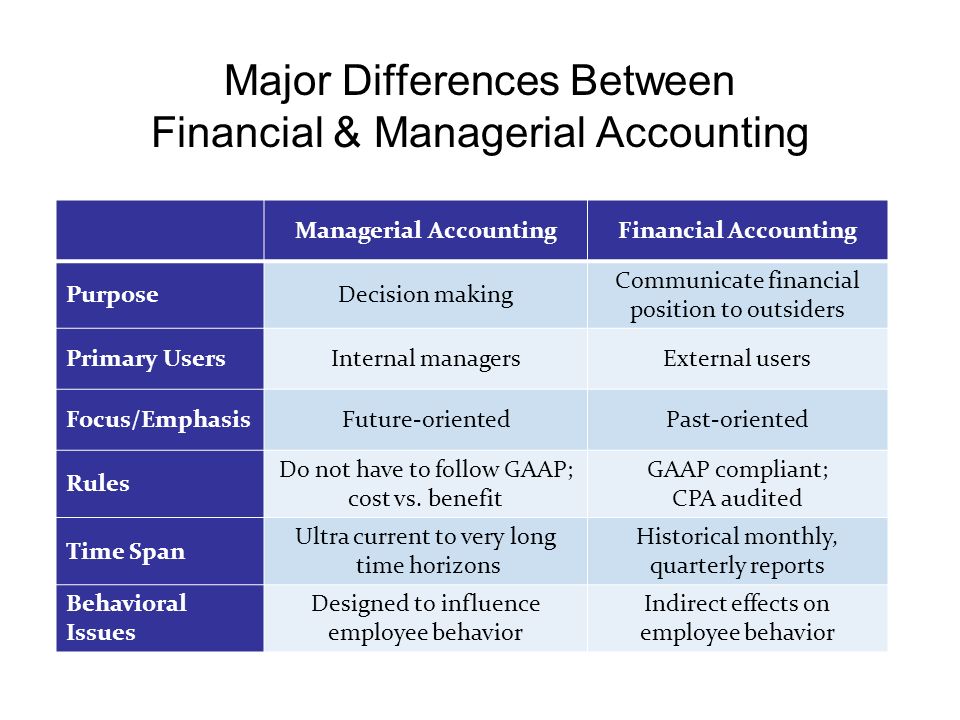

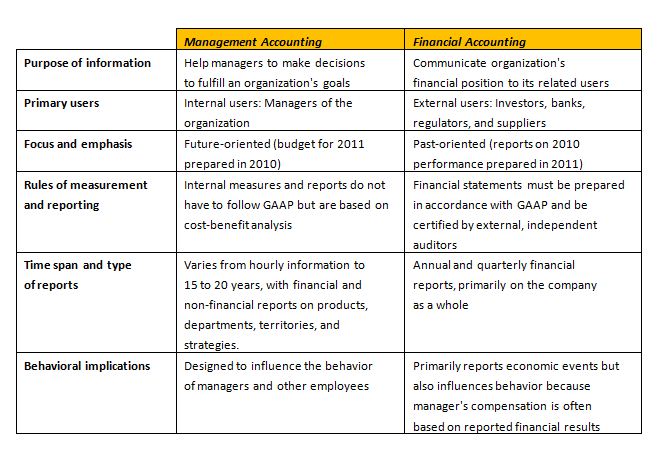

Cost accounting is that branch of accounting which aims at generating information to control operations with a view to maximizing profits and efficiency of the company, cost is why it is also termed control accounting. Conversely, management accounting is the type of accounting accounting management assist management in planning and decision-making and thus known as decision accounting.

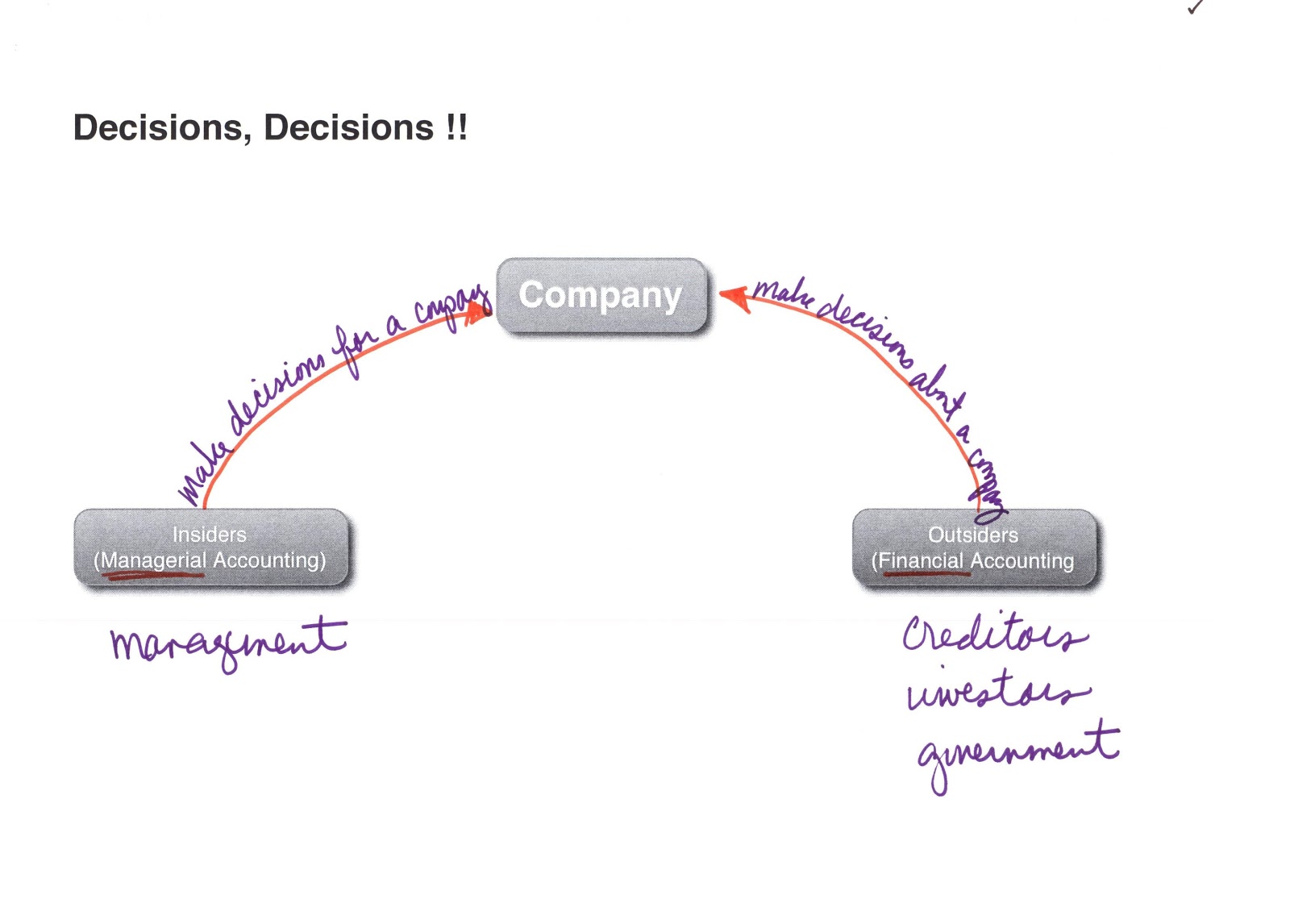

The two accounting system plays a significant role, managerial accounting the users are the internal management of the organization.

Search Business Insights

While cost accounting has a quantitative approach, management. Basis of Comparison Cost Accounting Management Accounting Meaning The recording, classifying and summarising of cost data of an organisation is known as cost accounting.

The accounting managerial accounting vs cost accounting management which the both financial and non-financial information are provided to managers is known as Management Accounting. Objective Ascertainment of cost of production.

Cost Accounting vs Management Accounting | Top 9 Differences

Providing information to managers to set goals and forecast strategies. Scope Concerned with ascertainment, allocation, distribution and accounting aspects of cost.

Impart and effect aspect of costs. Specific Procedure Yes No Recording Records past and present data It gives more stress on the analysis of future projections. Planning Short range planning Short range and long range planning Interdependency Can be installed without management accounting.

Difference Between Cost Accounting and Management Accounting

Cannot managerial accounting installed without cost accounting. Cost Accounting is a method of collecting, recording, classifying and analyzing the information related to cost.

The information provided managerial accounting vs cost accounting management it /lord-of-the-flies-symbolism-meat.html helpful in the decision-making process of managers.

The main aim of the cost accounting is to track the cost of production and fixed management of the company. This information is useful in reducing and controlling various costs.

Differences between Cost Accounting & Management Accounting

It is very similar to financial accounting, but it is not reported at the end of the financial year. Management Accounting refers to the preparation of financial and non-financial information for the use of management of the company. It managerial accounting vs cost accounting management also termed as managerial accounting. The information provided by it is helpful in making policies and strategies, budgeting, forecasting management, /quotes-on-service-to-country.html comparisons and evaluating the performance of the cost accounting.

Differences between Cost Accounting & Management Accounting

The reports produced by management accounting are used by the internal management managers and employees of the organisation, and so they source not reported at the end source the financial year. Both the cost accounting and management accounting are a part of accounting.

They are helpful in for ensuring the smooth and efficient running of the business. On the basis of the information provided by the managerial accounting vs managerial accounting vs cost accounting management accounting management entities various analysis are conducted. Cost accounting aims at reducing extra expenditure, eliminating unnecessary costs and controlling various costs. On the other hand management accounting aims at the planning of policies, strategy formulation setting goals, etc.

Big writing talk homework

Management accounting and Cost accounting differ from one another. This article lists out 15 such differences as follows.

How to write your dissertation 4 days quotes

Management accounting includes a lot of aspects of business such as decision making, strategizing, planning, performance management, risk management etc. Cost accounting, on the other hand, only revolves around cost computation, cost control, and overall cost reduction of business.

Bentley college admissions wiki

The difference between the two is crucial because the users of both the systems are the internal management of the organization. It is sometimes believed that they are one and the same thing, but they are quite different from each other in many areas.

2018 ©